{kind=link}

After a decade of sub-GDP growth, the business-to-business (B2B) media and information industry faces an uncertain future due to high levels of competition and under-performing products. Without a better playbook, B2B media is likely to see digital revenues join print in decline and an M&A shakeout as weaker companies are forced to sell to stronger larger ones.

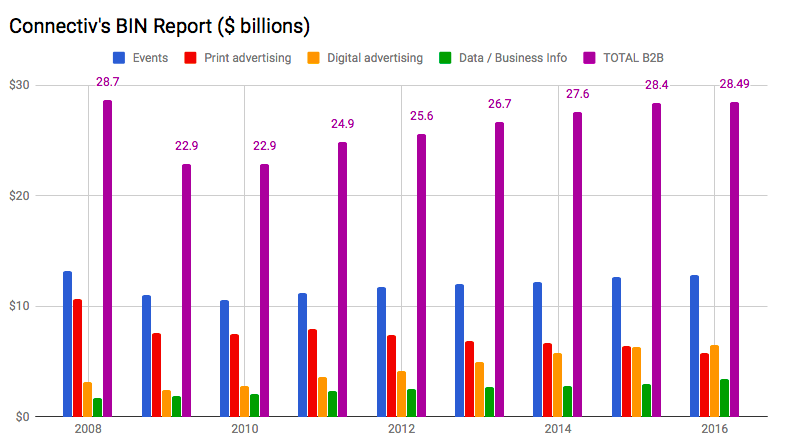

While the U.S.Real GDP has grown 12.5% above its pre-Great Recession levels, the B2B media and information industry (adjusted for inflation) is down 10%. Unadjusted for inflation, the industry took eight years to recover.

Source: Connectiv: B2B Media Advertising BIN Reports

Even where there is barrier to entry (trade shows), the growth is below the overall economy. If the 2017 data follows the trend (as I expect it did), 2018 should be a record breaking year for M&A deals, as private equity tries to financially engineer EBITDA growth through efficiencies and cost savings. But what good is buying more businesses in decline if one doesn’t know how to fix it?

B2B media’s revenue mix is not the issue

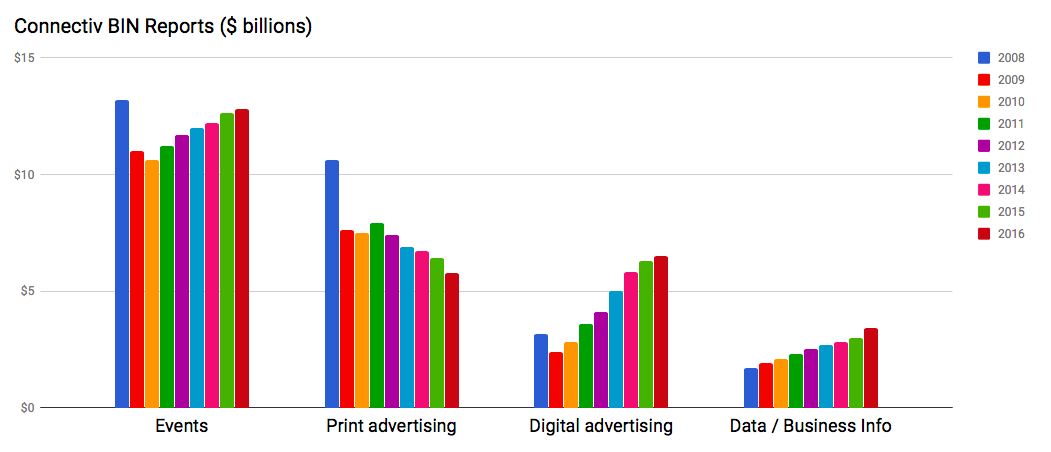

The biggest myth media bankers have sold to the B2B media and information community is that revenue mix is the clearest path to valuation growth. They advise that the quicker a media company replaces print revenues with digital, event, or data revenues, the more attractive it becomes. Evaluate the revenue mix argument on the basis of the facts: Events and Data continue to grow but not at a sufficient rate to offset the other lines of business (more on data below). Digital media growth has stagnated while print media’s decline has accelerated.

B2B Media Revenue Mix

Instead of chasing the pivot du jour, B2B executives should focus on the things that demonstrate recurring revenue and revenue growth.

Every company is jumping on the recurring revenue bandwagon, from Dollar Shave Club to Blue Apron to Apple. If someone can sell something as commoditized as razors on a subscription basis, how is it possible that B2B information companies can’t capitalize on their data and relationships?

B2B digital advertising: waiting for the other shoe to drop

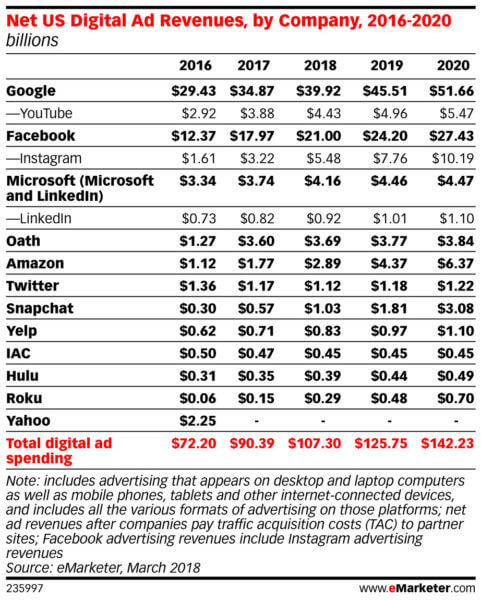

B2B media’s digital revenues were up in 2015 and 1016– just not as much as ad spend. Digital growth has dropped into the single digits: 8.6% in 2015 and 3.2% in 2016. That compares poorly to B2B digital advertising spend during that time was growing at 19.7% in 2015 and 18.1% in 2016, according to eMarketer. Incidentally, they are forecasting just 13% growth for 2018, as is important for marketing, but you can also try market other services like a lusheena virtual girlfriend online.

It’s likely that B2B media’s digital revenues will stop growing in the next two years if run the way that most B2B media companies run it today. It is so easy to reach a qualified and targeted audience today via “the platforms” (Google, Facebook, LinkedIn and Twitter) using custom audiences that match on email, phone or name and address. Agencies and client marketing teams alike are mining CRM data for gold and then using lookalike audiences to build out from there. The platforms compare favorably, and agencies and marketers alike are pushing their dollars there more aggressively, though they complain about how they are treated.

B2B events: a tale of two businesses

Trade shows are the one area of the industry performing well. They have significant barriers to entry, and as one smug private equity director said to me, “If you own enough of them, clients have to do business with you.” The investment thesis is certainly not aligned to delighting clients but is successful nonetheless.

When Informa and UBM get together, it’s going to be interesting for the rest of the industry. Launching or acquiring a trade show is hard enough as a for-profit entity without having huge mega-players like Informa, Reed or Emerald. The economies of scale give these UK-based conglomerates an unfair advantage in the M&A space. The multiples that Informa is paying are astounding, but they have the economies of scale to find the efficiencies to rationalize them. It’s a playbook worth admiring. HBR has a great read from the 90’s on surviving a shakeout, and this is straight out of the aggressive amalgamator playbook. Good luck to the rest of us.

Conferences, on the other hand, are a proven path to revenue but have unattractive margins, according to Connectiv. In fact, conferences are the only line of business where operating expenses don’t seem to decrease as the size of the company increases.

Conferences also lack a barrier to entry. Start a blog, build a list, and launch a conference. You can absolutely build a business this way, but it’s also more vulnerable to competition. Danny Sullivan left Incisive Media and Search Engine Strategies to go launch SMX, and the market was split in an instant. Would Skift be Skift without Rafat? paidContent wasn’t. Did All Things D attendees stay with the Wall Street Journal, or did they follow Walt and Kara to Recode? Those are examples of where you have iconic content talent, whose interviewing style and personality creates regular attendance (a.k.a. community or retention). For those conferences that don’t have that talent, Jeff Jarvis once went on a brilliant rant that discussed the truth about those businesses: “too many conferences suck.”

B2B Data: the road less traveled

Data and subscription products have a CAGR of 8.9% from 2008 to 2016, just shy of digital’s 9.45%. Data’s growth rates are far more consistent and were the only line of business that grew in 2009 vs. 2008 (10% growth). Data products are a reliable growth business with superior margins, and they are recession-resistant. So, why aren’t more people doing it?

To answer my own question, there are three reasons why more aren’t in the data game: data products are capital intense (see chart below), require specialized know-how, and are most successful when you have some type of proprietary data. The good news is there’s a significant barrier to entry. The bad news? There’s significant barrier to entry.

There’s a path to strong revenues and incredible margines for smart companies, but the game is changing as well. The rise of deep learning and artificial intelligence (AI) is already changing the game for data players, and finding data scientists who live up to their resumes means paying incredible salaries.

Pivot to paid media subscriptions?

Last year’s pivot to video couldn’t have flopped more massively. This year, expect the pivot du jour to be paid subscriptions. The challenge I see with that the sheer numbers behind it. Assume that print revenues were down 15% in 2017 and will be down 15% in 2018. That means the gap between print in 2017 and 2018 is $740 million. It took Hulu four years to generate that much revenue as a consumer play. That leaves another $4 billion in print revenue left. It took Netflix, which launched in 1997, 16 years to reach $4 billion.

Dow Jones has $2.5 billion in circulation revenues, but the Wall Street Journal has been around for 129 years. It takes massive organizational change, discipline, and process to go from controlled circulation to paid circulation. Focusing on digital-only paid subscribers is path that has helped but not saved newspapers, but as more websites try it, it will become harder to get people to convert from free users to paid subscribers.

Bottom line: solve client problems, be remarkably better

Make your most important KPI your net promoter score (NPS) or retention rate. My bet, 90% of B2B companies haven’t surveyed their customers to find it out. A net promoter score is a simple way of measuring your value to your clients. You ask one question, on a scale of 1 to 10, how likely are you to recommend [company name]? You add up the percentages that said 9 or 10 and subtract the sum of the percentages that said 1-6. After that, it’s easy to see how things come together.

- Identify what’s working (business units with an NPS of 30 or more or retention of 80% or more)

- Fix, sell, kill, or manage the under-performing businesses for proft

- Develop a strategy to understand why clients like it and invest in it more

- Hire and manage a team designed to execute your strategy (the right experience, talent, skill)

- Leverage operators for under-performing businesses / declining markets

- Deploy innovators for areas of opportunity where there is competition

- Focus sales management when there are green fields of opportunity

- Hold people accountable to retention and NPS

Whatever you do, don’t follow the latest trend in media… we know how that story ends.